Within the realm of options strategies, the term DTE0 has gained increased interest recently. Notably, applied to the S&P500 index in the United States.

So I did some research on this investment strategy and summarize here its main properties and reasons for its popularity.

- Options are very powerful and versatile financial instruments that allow implementing basically any pay-off profile one wants. However, they also involve (potential unlimited!) risk, if not only buying options but also writing (or selling) options is part of the strategy, as it is the case also for most DTE0 strategies.

- Liquidity is key for many forms of investing, hence the focus on the U.S. indices like the S&P500 (SPX).

- Options, when they were introduced at the CBOE in Chicago in 1973, where available with expiration only every quarter. Since then, maturities every month have been introduced and further weekly oètions expiring every Friday were added. In 2005, the “weekly” options were introduced allowing to trade options that expire on each Monday, Wednesday and Friday for major U.S. indices.

Information about this strategy can also be found on these two dedicated websites:

Bottom line, it is an options strategy based on statistical properties of the underlying stock index features.

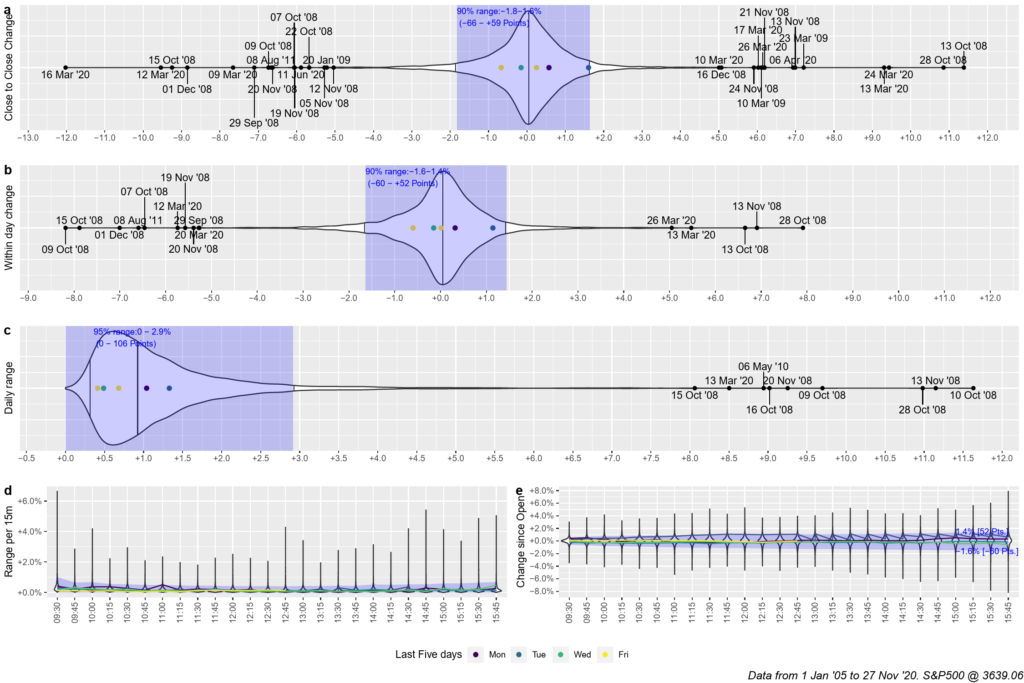

To start here I computed some statistical properties of the S&P500 over the last 15 years based on minute data:

The strategy is based on the ranges of the indeed throughout a day trading session. As can be seen from panel (c), the daily range over this period was in 90% of the cases about 100 points.

The strategy consists in setting up an Iron Condor (or Strangle, if buying power allows) of options +/- about this range around the opening value of the S&P500 and hold it throughout the trading day (from 9:30 to 16:00 EST) with the aim to let it expire worthless. Statistically speaking, in more than 80% of days, this strategy should lead to a worthless expiration of all options involved, leaving 100% of the premium received to the option seller.

Given an overall goal of about 90% success rate, the options to be sold should have a so-called DELTA of about 5 (or a 5% probability that they will expire in the money so that the option seller has to pay the option buyer the difference between market and strike price). Such 5-DELTA options of the SPX can expect a premium of about 0.5$ to 1.50$ in “normal times”. Given that options always involve a multiplier of 100 of the underlying, this means by selling one option on either side (PUT below the market price and CALL above the market price) will result in 2 x 1$ x 100 = 200 $ of option premia, which is before fees and taxes the maximum return of this strategy.

In the following posts, I will evaluate this strategy further.